Market report 10.06.2022

Osterhorn, Friday, 10.06.2022

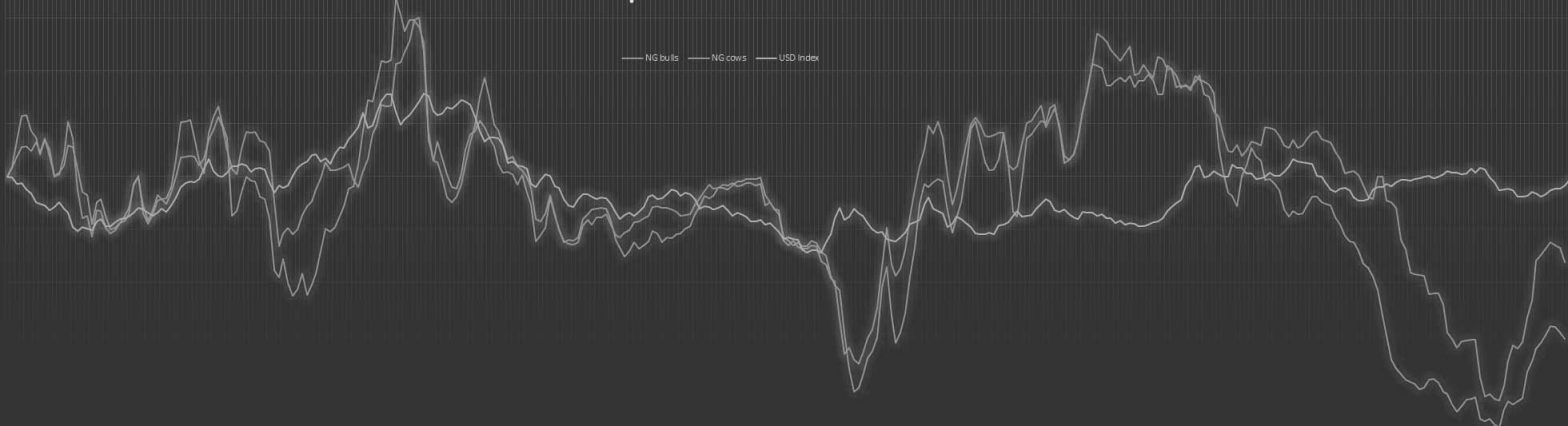

The US $ in EURO 1,0530

What happened this week

Another week has come to an end and the first half of 2022 is slowly drawing to a close. Who would have thought at the beginning of January what would happen in the following six months? Probably two things can be said for the moment. First, no one would have actually expected a new war of conquest in Europe and, consequently, the realisation that politics and economics are no longer really capable of managing crises or were prepared for them. Certainly, the leather market is affected by all these events, but actually the effect on the basic problem is rather insignificant. For some years now, leather has no longer been a necessary basic material whose demand is accompanied by the usual fluctuations in the consumer goods markets. The resulting effects have not yet really been internalised by all those involved. Thus, the usual stories continue to be told, always in the same hope that it will influence the market for the next few weeks and support the respective interests in buying and selling accordingly. The principle of self-fulfilling prophecy may work in normal times now and then, but it is certainly not a tried and tested procedure in disfunctional moments such as at present. All in all, what is happening at the moment is A) what one would expect and B) what is actually perfectly normal for the time of year. The leather industry in the Northern hemisphere is more and more preoccupied with its summer holidays. The whole environment is not encouraging many tanners at the moment to come up with solutions for the hides produced from late July and in August. Actually, people are obviously very content to take a break from the market for a few weeks

and, if necessary, use the opportunity to reduce stocks. Normally, one would perhaps expect that the falling prices could be used more as an opportunity to stock up for the second half of the year, but this is not really noticeable, at least until now. Only in Asia can one see this kind of routine. There has been some interest and enquiries this week, but the bid prices simply do not fit into our currently still valid price grid. There are sellers in other European countries who are able and willing to sell at much lower prices than ours, and this is of course used as a reference for what they would be willing to pay for our material. However, with the current prices at the slaughterhouses, this cannot be realised in any way. This really only leaves the decision of whether one expects better times and prices or whether one thinks that today’s loss might be the better one for the next months. Apart from that, other topics are coming more and more to the foreground again. Even if one does not like to talk about it openly overall, one notices that the leather industry obviously has to plan its cash-flow much more precisely again in view of the reduced summer revenues and the strongly increased costs. Even if there are no serious problems yet, the payments are not coming in at the same speed as they used to in the last few years. Business and sales this week were rather below average. While we in Europe are currently waiting for the new deals for the coming month, the prices received from the overseas markets were simply not workable. These were not small differences either, but 20 or more percent were not uncommon. This meant that sales remained very sporadic and limited to individual deals.

The kill

There is not much news to report on the kill. It is just plodding along, the cold stores are well filled and demand for prime cuts is simply too low. Live cattle prices continue to fall and it is hoped that the price relief will eventually revive demand for the holiday season and the restaurant business.

What do we expect

We are now shortly back to the next round of buying and pricing at the abattoirs. The outcome will most certainly affect the trend and business for longer than just the usual next few weeks. Without a serious adjustment to the world market and the possibility to squeeze out other suppliers via price, sales opportunities will probably remain limited. The only hope for a real revival of demand can really only be had for Asia, provided that prices there are considered speculative, attractive for the second half of the year. However, this is only really possible if one is prepared to actually be able to calculate the corresponding offers, because otherwise the only thing that helps in the end is to wait and see.

| Type | Weight range | Avg. green weight | Salted weight | Avg. weight salted | Price per kg green weight |

Trend |

|---|---|---|---|---|---|---|

| Ox | Heifers | 15/24,5 kg | 22,0/23,5 kg | 13/22 kg | 20/21 kg | € 1,20 | Stable |

| 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,80 | Weakish | |

| Dairy cows | 15/24,5 kg | 22,5/23,5 kg | 13/22 kg | 20/21 kg | € 0,70 | Weakish |

| 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,65 | Weakish | |

| 30/+ kg | 33,5/35,5 kg | 27/+ kg | 29/31 kg | € 0,60 | Weakish | |

| Bulls | 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 1,20 | Weak |

| 30/39,5 kg | 36,0/37,0 kg | 24/34 kg | 31/33 kg | € 1,35 | Weakish | |

| 40/+ kg | 45,0/48,0 kg | 34/+ kg | 38/40 kg | € 1,30 | Weakish | |

| Thirds | 15/+ kg | 25,0/27,5 kg | 13/+ kg | 24/26 kg | € 0,50 | Stable |

| Thirds bulls | 30/+ kg | 38,0/40,0 kg | 24/+ kg | 33/36 kg | € 0,50 | Stable |